TMAD Flow: Why CPI May Be Misleading

$DELL $SNOW $SPX

Hi everyone,

On the surface, the numbers were reassuring. Energy prices, particularly gasoline, pulled the headline figure lower. Core inflation (ex-food and energy) printed at a flat 0.0% month-over-month.

However, today’s CPI data suggests the economy may be closer to the verge of deflation than inflation — and that is a real concern. The distinction matters:

Inflation can usually be controlled through monetary policy.

Deflation, on the other hand, is a completely different problem. It typically signals severe underlying economic weakness.

These one-off suppressions (and the deflationary tilt we’re seeing) won’t last.

What’s Coming Next

July CPI (released August 12): Headline may look tame thanks to lingering low gasoline prices. Markets could breathe a sigh of relief.

Core inflation, however, is likely to re-accelerate as distortions normalize.

By August/September, base effects reverse. Oil prices are rebounding amid geopolitical tensions. Adding fuel to the fire: Ukraine is damaging Russian refinery facilities, and Putin has blocked diesel exports to limit domestic shortages.

Worse still, with oil flows restricted through the Strait, diesel — the most impacted fuel — faces severe pressure. It takes roughly 3 barrels of crude oil to produce 1 barrel of diesel. When barrels don’t flow freely, shortages intensify quickly.

This combination is setting up a major supply shock in refined products, which will likely push energy prices and bond yields toward new highs.

The result? A hotter-than-expected inflation print that could jolt complacent markets.

Structural Headwinds

Valuations remain stretched (SPX forward P/E ~20+).

The AI boom is driving massive electricity demand, feeding into higher energy costs and core inflation.

Tech giants are spending hundreds of billions on data centers, much of it debt-financed. Rising yields would hammer their valuations and ROI.

Low volatility and concentrated market leadership (especially semis) create classic conditions for a sharp correlation shock if inflation surprises to the upside.

How Will We Protect Ourselves

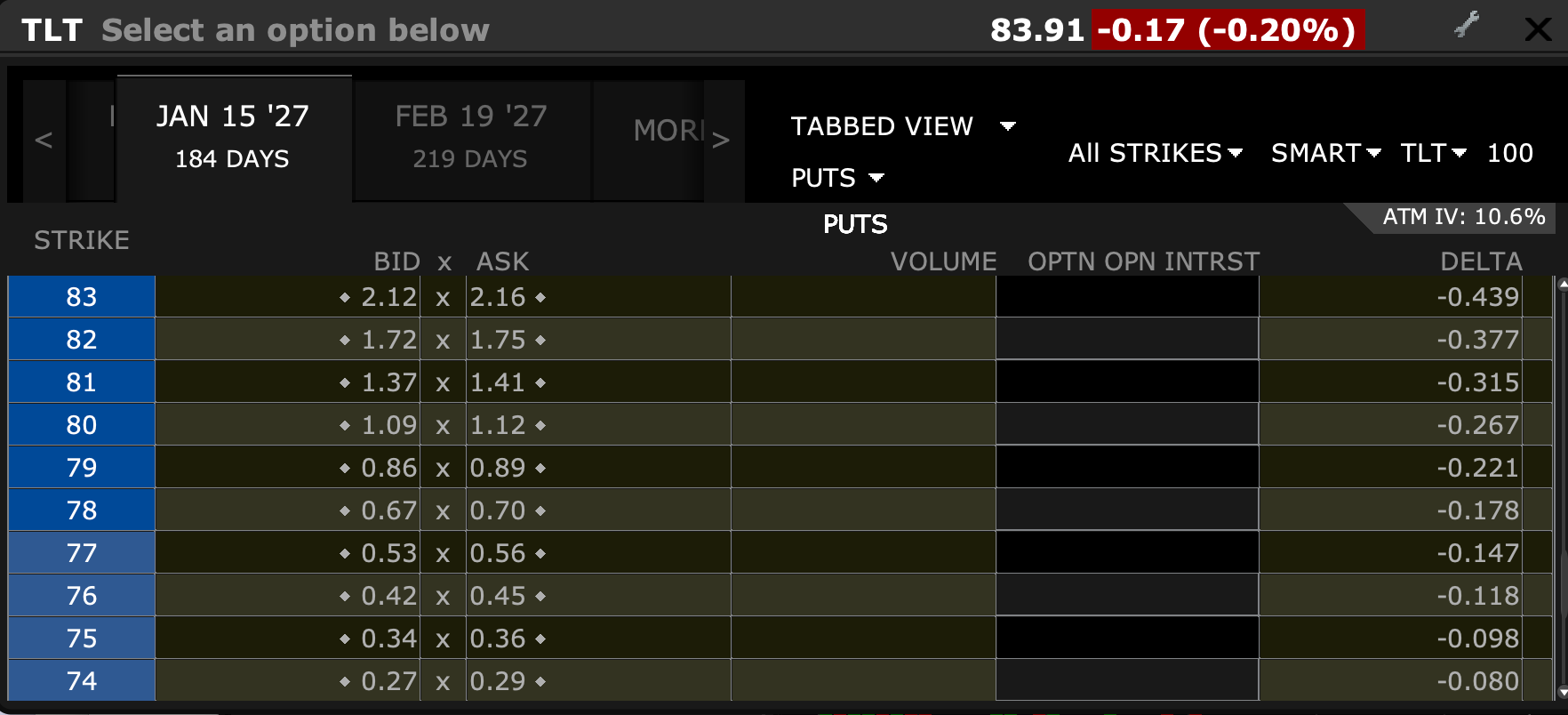

Buy some OTM TLT puts, 2027 expiry

78 and 76 strikes for January 15, 2027.

Bullish on energy and nuclear into fall — the clear winners from sustained electricity inflation.

Some SPY/QQQ put spreads with November/December expiry.

We stay away from overpriced AI names, max. trade them short term if we see a good setup/momentum.

Bottom Line

CPI data may lull investors into complacency. But the pieces are aligning for a yield spike and a market wobble later this summer and early fall. Warsh’s comments were a clear warning shot.

It doesn’t mean we’re bearish quite yet. We will play names with good momentum in the short term and keep some cash for a potentially wacky end of August/September.

IBM had its worst day in 40 years, ending the day with over a 25% loss.

Our scanner saw HIGH PUT GEX on Friday and Monday, a warning sign. You all have access to the TMAD App. Always good to double-check and see what options are showing. Hope none of you was in this name.

Now, let’s look at SPX levels and some more trade ideas: